Dear friends,

Welcome to the May issue of Mutual Fund Observer. We’re glad you’re here.

May marks the end of my 40th year of teaching at Augustana College. (And no, they’re not free of me yet. I’m back again in the fall!) It’s an amazing place that has grown a lot over the course of my career. We were founded in 1860 by educated immigrant parents who were anxious to preserve the traditions of their (Scandinavian) homelands while helping their children compete in a strange new world. We were a small school dedicated to helping the children of immigrants … and their native-born neighbors.

In 1984, when I arrived, we were “an A+ school for B+ students.” Today we’re a college that has a legitimate international draw – nearly 20% of our incoming class are international students – and an ongoing sense of social responsibility: 22% of our students come from low-income families, 22% are first-gen students, 23% are domestic students of color.

I wanted to mention all of that as a way of reassuring folks who’ve been watching news of startling protests at a handful of high-visibility colleges in the past couple of weeks. You’ve seen rowdies and buildings occupied and the insanity of sending riot police onto campuses. That’s horrifying.

But that’s not actually the life of college students across the country. At Augie and the many other schools I have contact with, life is about the rhythm of the end of an academic year. Final exams. Angst about jobs and friends and internships. Hopes for the summer and the seasons beyond. It’s about capstone presentations and Last Lectures. It’s about training Viking Pups, a student-led effort to train service, facility, and therapy dogs. It’s about a bunch of stuff that would make you insanely proud and hopeful, but which never warrants much attention.

Be of good cheer, dear readers. We are – one and all – more sensible than we’re led to believe.

In this month’s Observer

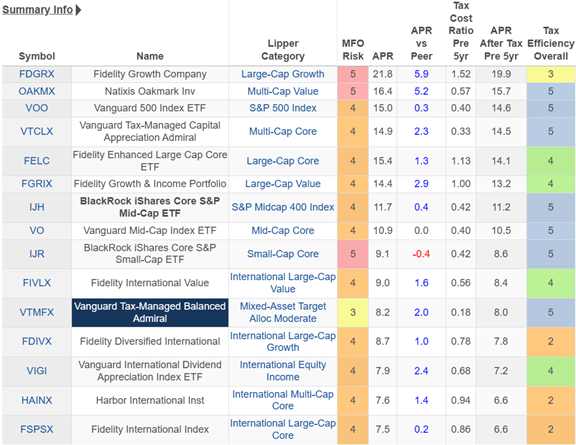

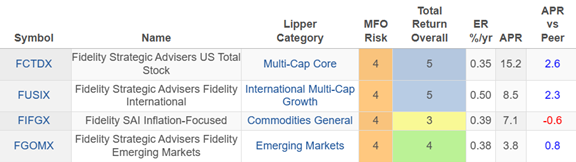

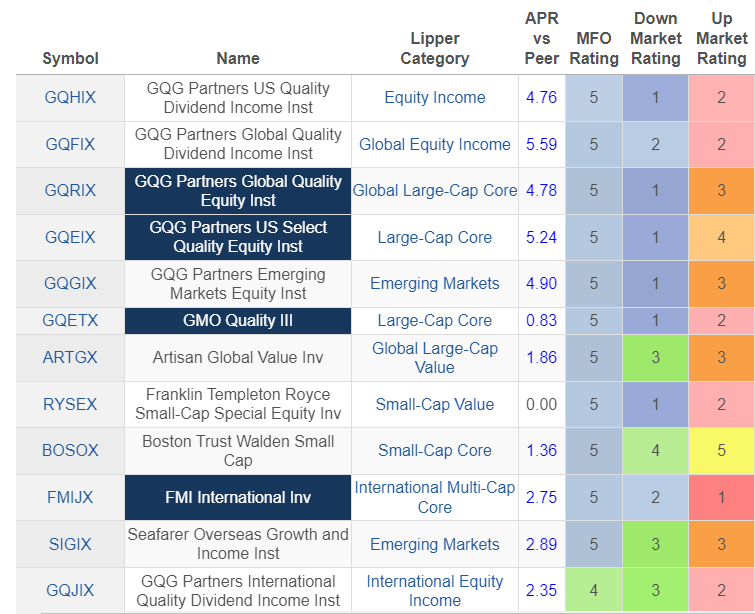

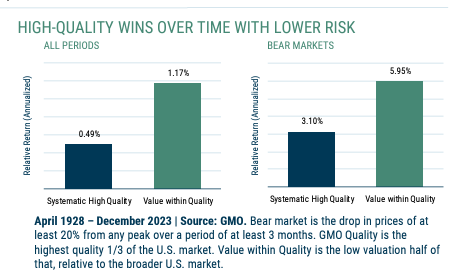

We’re packing a remarkable number of funds into just a handful of articles. Lynn Bolin looks at strategies for tax-efficient investing. The Shadow works through another dozen stories of change in the industry. And, in a first, we’ve partnered with the folks at Morningstar to think quality thoughts. I walk through “the quality anomaly,” the persistent pattern in which funds investing in high-quality stocks have both higher returns and lower volatility than the market. We recommend two funds that represent core holdings for investors interested in profiting from the quality anomaly while Robby Greengold of Morningstar offers up a dozen more that might serve to round out a portfolio. In addition, we profile one of the newer members of Rajiv Jain’s GQG family: GQG Global Quality Dividend Income Fund, a fund for equity investors facing a “higher for longer” world.

What’s in a name?

Many parents give their children names that express their hope for a bright future (“Prince”) or to help them stand apart (“X Æ A-12 Musk”), as well as to honor family traditions or long friendships (I’m named after our family doctor, for instance). There’s a rich field of research into the effects of naming, including the finding that girls with gender-neutral names (“Alex” rather than “Isabella”) are more likely to persist in, and thrive in, traditionally male-dominated fields; that easy to pronounce names are associated with greater likability and likelihood of professional advancement, while names that are seen as hyper-distinctive, hard to spell or hard to pronounce tend to be associated with exceptional life challenges.

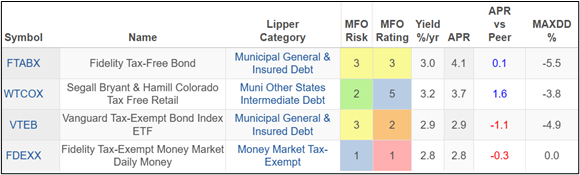

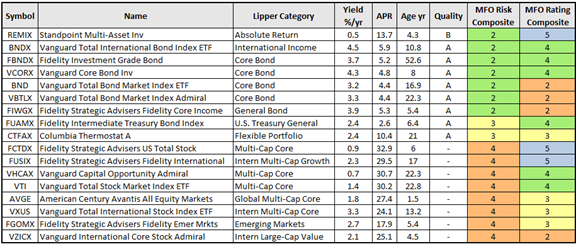

This is my way of saying, “Sorry for ignoring you Penn Mutual AM 1847 Income Fund (PMEFX). You deserve better but, really, I thought you were some sort of insurance product. Maybe some sort of bonds-plus portfolio? “Blame it on the name.”

PMEFX was commended to me by an MFO reader, shipwreckedandalone, who wondered why we hadn’t paid attention to it. When I asked what drew their attention to the fund, they replied,

Cipolloni managed Berwyn Income before the buyout. Lee Grout had a stock-picking process at Berwyn. PMEFX uses high-yield corp credit. B and BB securities mostly. Holds nothing below B. Shorter duration. Key to strategy is to stay with smaller issues with more cash than debt on the balance sheet. Free cash flow positive holdings. Convertible bonds. He prefers bonds with change of control provisions. 33% equities. Mostly small caps. Bottom line …he prefers “yieldy” holdings bonds and stocks with income while not allowing large drawdowns which is my portfolio objective. Outperformed the iconic VWINX in every metric since inception. I also like his age…will not be retiring soon and force me to make a decision. Thank you for this website, great source of info.

Well, okay then! You had me somewhere between “Berwyn Income” and “outperformed Vanguard Wellesley Income,” a five-star, $50 billion fund.

So, let’s unpack things. There was a very distinctive boutique fund named Berwyn Income. Because it’s hard running a tiny shop, Berwyn was sold to Chartwell. The fund continued under its old name, team, and strategy. Morningstar’s Patricia Oey in 2018, after the sale of Berwyn to Chartwell but before the disappearance of the management team:

Berwyn Income is a solid option for investors comfortable with a flexible and contrarian conservative-allocation strategy. The fund has a disciplined process, below-average fees, and good downside protection.

Over Cipolloni’s tenure as manager, the fund has turned in impressive results, outpacing the allocation– 15% to 30% equity Morningstar Category by 2.7%, annualized, through November 2018. And over the past decade, the fund’s risk-adjusted returns landed in the category’s top decile. This performance was achieved through asset allocation and security selection, which illustrates the capabilities of this small team.

Investors here remain in good hands (December 7, 2018).

But not for long. In March 2016, Berwyn’s long-time adviser, Killen Group, was sold to Chartwell Investment Partners. One condition of the sale was that Mr. Cipolloni and the team remain for three years. They did. Then, three years and a day later, they left. We noted in March 2019, three months after Oey’s analysis, that

The unexplained departures of Messrs Cipolloni and Saylor from Berywn Income (BERIX) is a game-changer and a fund changer. The pair had been managing the fund together for a dozen years with a distinctive go-anywhere approach. They departed rather abruptly in February, causing Morningstar’s analysts to downgrade the fund and Morningstar to declare it to be “a new fund.”

When the team left, Chartwell chose to rename the fund Chartwell Income and incorporate two of their other strategies into the rechristened fund. Chartwell itself was sold in 2022 to Carillon Tower Advisors, which shifted its focus again. In February 2024, the fund became Carillon Chartwell Real Income, a TIPS fund. So, the ticker symbol BERIX lives on, but the old fund does not.

Except that it does, as the Penn Mutual AM 1847 Income Fund, run by the Berwyn Income team. Remarkably, it even charges a little bit less than it did years ago when it was a much larger fund. The only notable difference from the original is that 1847 can own 40% stocks rather than 30%.

Driven by a bottom-up, value-based investment process, the Fund employs a flexible asset allocation with a 40% common stock limit (at purchase) balanced with investment-grade corporates, high-yield bonds, convertible bonds, and preferred stock. The goal is to produce sustainable income and positive total returns in excess of the category average over a full investment cycle.

The managers stress their commitment to limiting downside risk, avoiding overheated sectors, and pursuing asymmetric opportunities:

our “willingness to go where we see value, move against the crowd and avoid obvious risk are other key hallmarks that guide the Fund through most market environments. This strategy requires a common sense approach to ensuring that for each investment made in the portfolio that we are getting, in our opinion, a reasonable potential return without accepting more risk than necessary. Simply put, if we do not believe we will receive an adequate amount of compensation/total return for the risk we are assuming, we will wait. And if our data shows that we are receiving a good balance of potential reward versus risk, we will act. This philosophy has helped to avoid making big mistakes by staying away from overheated/overvalued markets and investing aggressively when the odds and value are in our favor.”

The team did, indeed, excel in the face of a series of near-catastrophic years including 2008.

Since inception, the 1847 fund has outperformed Wellesley as well as both conservative and moderate Lipper peer groups. Morningstar designates it as a four-star fund.

| APR | Max DD | Sharpe ratio | Ulcer Index | Downside dev | Yield | |

| PMEFX | 2.5 | -12.4 | -0.3 | 4.5 | 6.1 | 4.6% |

| Vanguard Wellesley | 2.1 | -14.7 | -0.07 | 6.7 | 7.0 | 3.4 |

| Conserv alloc | 0.9 | -16.8 | -0.22 | 8.7 | 6.7 | 2.4 |

| Moderate alloc | 3.0 | -19.7 | 0.02 | 9.6 | 8.3 | 2.0 |

On the whole, Penn Mutual AM 1847 Income Fund deserves more investor attention … and a much snappier name.

The ARK is taking on water

![]() Apropos our discussion of quality investing, investors are increasingly voting with their feet when it comes to the high-profile / low-quality portfolios offered up by ARK Investments. Cathie Wood’s shop has seen $2.75 billion in outflows in the past 12 months including pulling “a net $2.2 billion from the six actively managed ETFs at her ARK Investment Management this year, a withdrawal that dwarfs the outflows of 2023” (“Wood’s Popular ARK Funds Sink, Investors Withdraw $2.2 Billion,” Wall Street Journal, 4/24/2024, p 1). A palindromic date: 4/24/24!

Apropos our discussion of quality investing, investors are increasingly voting with their feet when it comes to the high-profile / low-quality portfolios offered up by ARK Investments. Cathie Wood’s shop has seen $2.75 billion in outflows in the past 12 months including pulling “a net $2.2 billion from the six actively managed ETFs at her ARK Investment Management this year, a withdrawal that dwarfs the outflows of 2023” (“Wood’s Popular ARK Funds Sink, Investors Withdraw $2.2 Billion,” Wall Street Journal, 4/24/2024, p 1). A palindromic date: 4/24/24!

Derided as “more vulnerable than visionary” by Morningstar, her flagship fund is down 14% YTD. Its relative returns in the past five years, including 2024: top 1%, bottom 1%, bottom 1%, top 1%, bottom 1%. Morningstar’s snapshot of the quality of the stocks in the portfolio is telling:

Global X boards The Trump Train

According to Morningstar, Global X Social Media ETF (SOCL) is the fifth fund to board the Trump Train. A bit over 1% of the ETF’s portfolio is invested in Trump Media (DJT). Morningstar now estimates the stock’s fair value at $70 / share, trailing 12 month revenues of $4 million.

In celebration of two anniversaries

This month marks the 12th anniversary of the launch of the Mutual Fund Observer, a site dedicated to carrying on and building on, the tradition of FundAlarm.

We’ve been honored by the company of two-and-a-half million readers over the years, as well as by the work of a team of amazingly talented volunteers (Charles Boccadoro, maestro of MFO Premium; Ed Studzinski, curmudgeon-at-large and former co-manager of Oakmark-Balanced; Devesh Shah, co-creator of the VIX index; Lynn Bolin, retired engineer, Habitat volunteer and data maven; The Shadow, whose true identity is unknown even to those closest to them, and a dozen more) and the amiably disagreeable denizens of the MFO discussion community. Thanks, blessings, and cheers to you all.

Today also marks the one-week anniversary of Chip and my marriage. On Friday, April 26, 2024, we were married in a small civil ceremony in the company of our sons and two old friends.

Chip has been my constant companion for the past 14 years, and the source of more joy and comfort than you could imagine.

Thanks, as ever …

To our faithful Regulars and to the happy reinforcements offered by this month’s Irregulars! The rhythm of life hasn’t allowed us a honeymoon. As her college’s chief information officer and information security lead, Chip needed to attend the Educause Conference in Minneapolis this week. I tagged happily along, writing from an ancient laptop perched on a hotel room table. We’re debating whether it’s our conferencemoon or honeycon. In any case, we’re rather short on resources.

In our June issue, we’ll happily recognize this month’s supporters by name. Heck, if you’d be willing to share a selfie (or a selfie of your favorite pet), we’d include that too. And if anyone else would like to crowd that happy and generous crew, please consider supporting MFO.

In mid-May, I’ll be joining an investor retreat with the folks from FPA while Devesh meets the Artisan gang. Let us know if there’s something you’d like us to raise with them. In June, I’ll be attending the Morningstar Investment Conference at the Navy Pier. That should be interesting. Wave if you’d like to find time to chat.

Also in June, our long-brewing article on infrastructure investing and two fund profiles!

See you then!